Tokenisation: Revolutionising the Funds Management Industry

Tokenisation: Revolutionising the Funds Management Industry

Could digital tokens disrupt a $100+ trillion industry?

Hi readers, welcome to my first article of 2022. I’ve spent the past couple of months doing a deep dive into the world of NFTs, exploring developments in the metaverse and Play-to-Earn gaming, and learning about the economics behind digital tokens (‘tokenomics’). I look forward to sharing my learnings on these various topics with you all in the coming weeks.

Today, however, I wanted to focus on the concept of ‘tokenisation’.

As a young professional in the funds management industry, in the past few months I have become increasingly fascinated by, and passionate about, the ways that distributed ledger technology and digital tokens could revolutionise the way the entire industry works.

I will use this article as a way of laying out my thoughts in layman’s terms, and hopefully in the process get a few of you (especially my colleagues in the industry) excited about how tokenisation could change things!

What the heck is funds management?

Funds management, also commonly known as asset management or investment management, largely refers to the industry of companies that provide investment services and manage investments for clients.

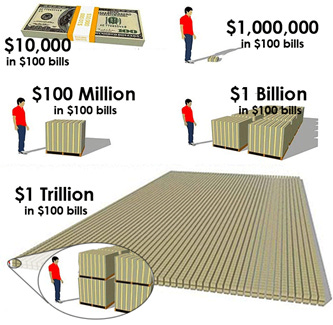

According to a Boston Consulting Group report last year, the funds management industry is a $100+ trillion behemoth. Its hard to even wrap our heads around just how much money that is. Here’s a cheeky graphic to put it into perspective.

Some examples of funds management companies include BlackRock, Vanguard Group, Fidelity Investors and State Street Global Advisors.

Based on the particular investment agreement, a fund manager will generally invest in stocks, bonds or other assets like real estate. Some fund managers specialise in just a couple or even just one asset class, e.g. real estate.

In the context of funds management, an investment fund (mostly just known as a fund) is basically a pool of money from different investors, managed by the fund manager. These funds can often be thought of as a ‘wrapper’, since investors own units in a fund, which in turn might own (through some sort of legal structure) a portfolio of various assets (e.g. a real estate fund might own 25 different buildings).

Investors in these funds can be institutional investors (large, sophisticated investors – e.g. pension funds or superannuation funds), or retail investors (typically smaller investors, e.g. ‘mum and dad investors’).

Oftentimes, there are funds that only institutional investors can access, and funds that are mostly designed for retail investors. Where there are a bunch of institutional investors or retail investors in a single fund, we call these pooled funds. Probably the most known type of pooled fund today is the ETF (‘exchange traded fund’), which tracks stock indexes like the S&P500.

On the other hand, sometimes a large investor (think: institutional or very high net worth) might have very specific goals. These investors may choose to have an investment team tailor a ‘bespoke’, personalised portfolio just for them.

How does the average Joe invest in one of these funds?

There are generally three main ways retail investors can invest in one of these funds:

1. Directly

An investor goes to the fund’s website, reads the offer documents, and submits an application

2. Through a fund platform

A platform lists lots of different funds you can invest in

This method isn’t always available, and is common with ETFs

3. Through a financial adviser, who then uses a fund platform only available to advisers

In many funds, investors can only go direct or through a financial adviser to invest in a fund.

Ok so what exactly is tokenisation?

Tokenisation refers to ‘digitising’ assets, i.e. converting the traditional units in an asset into digital tokens.

Through using digital tokens, ownership in an asset (e.g. a building or an investment fund) is simply recorded on a distributed ledger.

We actually call these digital tokens ‘security tokens’ since their value is ‘secured’ by a real-world asset.

The security tokens are effectively ‘shares’ or ‘units’ in the asset that are stored and transferred between people on a distributed ledger/blockchain.

Note that a blockchain is just a type of distributed leger. In fact, all blockchains are distributed ledgers, but not all distributed ledgers are blockchains.

For a refresh on blockchains vs. distributed ledgers, check out this article

When we talk about tokenisation in the context of funds management, we’re talking about using blockchain-compatible security tokens to represent ownership in a fund (the tokens are ‘secured’ by the value of the investments in the fund, e.g. all the stocks or real estate the fund owns).

Are tokens the same as cryptocurrencies?

No! They are actually a completely different type of digital asset.

Cryptocurrencies are the native tokens of a blockchain. Tokens are built on top of a blockchain.

As an example, Ethereum is a blockchain, and its native token is ether (ETH). Ether is the cryptocurrency for the Ethereum blockchain. Meanwhile, lots of different projects use the Ethereum blockchain. The digital assets of these projects are what we call tokens (i.e. they are not cryptocurrencies).

What’s so great about tokenisation? What’s this got to do with funds management?

Here are a few main ways that using distributed ledger technology can improve the funds management industry:

It can save the fund manager money

It can improve the investor experience

It can help the fund manager do their job better

Below are some examples of each point

Saving the fund manager money

There are a lot of stakeholders involved in the actual operation of a fund. There are investors, financial advisers, distributors, ratings agencies, fund platforms, custodian banks, registry providers, order-routing networks, fund accountants and fund managers.

Within this complex ecosystem, a couple of key processes that tokenisation can improve include:

1. Tokenisation can eradicate the need for a centralised unit register

Using a distributed ledger, transactions in the fund (e.g. a new investor coming in, or an investor withdrawing their money) would be instantly recorded on the ledger

Registry providers (sometimes known as transfer agents), who currently update unit registers for funds, wouldn’t have to do this anymore since it is done automatically by the ledger

2. Tokenisation can remove the need for duplicative record-keeping and reconciliations

The ledger becomes the one source of truth. Various stakeholders (custodian banks, registry providers and fund accountants) no longer need to reconcile their books with each other.

This would eliminate inaccuracies (and the costs of correcting inaccurate records), as well as save considerable amounts of time given the data is available to all parties instantly

Improving the investor experience

1. Tokenisation can lower the minimum investment requirements of a fund

Digital tokens can be considerably ‘fractionalised’ (i.e. split into lots of units). The operational efficiencies of tokenisation can allow for reductions in the minimum investment amount in a fund, meaning that people can invest amounts they might be more comfortable with

This is useful as many funds currently have a considerable minimum investment hurdle of e.g. $10,000

This could widen the potential investor base of the fund, so when the fund manager chooses to do a capital raise, they have more options (i.e. lowering the minimum investment hurdle considerably benefits the fund manager as well)

2. Tokenisation can help retail investors access more bespoke, tailored investment portfolios

Given the lowering of minimum investment thresholds, retail investors can more easily achieve diversified portfolios that more closely align with their goals

In this way, funds management companies that offer tokenised funds can help investors better achieve their goals

3. Tokenisation can make settlement much faster

Digital tokens benefit from T + 0 settlement both for subscribing and redeeming investors. This means the transaction is processed on the same day, often in a matter of seconds or minutes.

Current banking systems often facilitate T+2 or T + 3 transactions, i.e. it can take 2-3 days for investor’s money to get deposited in the fund, or for the investor to get their money back once their redemption request is approved by the fund manager

4. Savings on operational efficiencies could be passed onto investors

Fees on tokenised funds could be lowered, giving tokenised funds a competitive advantage over their non-tokenised competitors

Helping the fund manager do their job better

1. Tokenisation can greatly improve fund managers’ access to data

Fund managers would have immediate access to the distributed ledger and would be able to access real time insights into cash inflows and redemption requests. Faster access to investor-level insights can help fund managers act and make decisions quicker

Currently there can be significant waiting periods (in many cases weeks) for reports from intermediaries on cash inflows and outflows, and investor behaviour. In a tokenised model, fund managers would not be as reliant on third parties for access to data insights

2. Tokenisation will force registry providers to think up new services to provide to stay relevant

Registry providers, who are largely responsible for maintaining the unit register in today’s system, would be forced to adapt and provide new services to avoid being made redundant

This could lead to greater analytics services being developed for fund managers, which would lead to more efficient and informed decision making

The dream of Secondary Markets for fund tokens

The above benefits outlined are reason enough for funds management companies to start seriously looking into tokenisation.

However, the real pièce de resistance is that tokenisation could lead to the formation of liquid secondary markets for tokens in funds. This could very well revolutionise the global financial system.

Many funds, particularly those that own real assets (real estate and infrastructure), are fairly illiquid in nature. This means that it can be hard for investors to get their money out when they want.

In fact, many investment mandates provide fund managers with the opportunity to withhold redemptions altogether, and often it can take many months for investors to receive their funds back.

An active secondary market for fund tokens would mean that, rather than waiting for the fund manager to repay their funds (which could take weeks or months), investors could simply sell their tokens in the marketplace.

The vast benefits of secondary markets for fund tokens could include:

1. Investors can sell when they want, and get the value of their tokens back immediately

2. Fund managers may not have to sell assets or refinance loans to cover redemptions as often

Rather than redeem their investments (i.e. the fund manager pays the investor back), the tokens could simply be recycled to another investor through trading on the secondary market

As a result, there could be less redemption requests

3. The value of assets under management could stabilise

Once investors can sell tokens rather than redeem units, there would be less pressure on assets under management, which could allow the fund to focus more on growth

4. Investors could allocate more money to previously ‘illiquid’ sectors like real estate and infrastructure, and benefit from the returns

Increased liquidity could mean that a greater % of investment portfolios could be allocated to these sectors, since investors don’t need to worry as much about not being able to get their money out

Investment portfolio managers would be able to rebalance client’s portfolios more frequently as they see fit, meaning a better overall experience for investors that better optimises for returns

5. There would be greater transparency of fund performance relative to competitors

A secondary market for tokens, e.g. the “Australian Fund Exchange” would bring the details around different funds to one place, in the eye of the public

Investors would be more readily able to compare the performance of different funds

Greater transparency would create significant competitive tension between fund managers to drive performance, ultimately benefiting investors

The Round Up

It’s pretty clear that tokenisation could bring tremendous improvements to the funds management industry. The potential for secondary markets down the line is immense.

However, we must note that there are significant complexities to address. Tokenising funds will take time. It requires shifts to digitisation across all key intermediaries (who will likely adapt to meet customer demand). Importantly, the regulatory frameworks around tokenising funds remain somewhat murky, especially across different jurisdictions. Work must be done to address this.

Nevertheless, the benefits of tokenised funds are so great that it would be rather short-sighted to do nothing now. Already, global asset managers like UBS Asset Management have completed proof-of-concept projects around using distributed ledger technology.

The risk for fund managers doing nothing today is that they will be behind the competition when distributed ledger technology becomes the norm. The process of implementing tokenisation will not be an overnight task.

About the author

I am a young property investment professional at AMP Capital. Outside of work I enjoy all all things investing and crypto, playing poker, basketball, getting outdoors and keeping fit.